Abstract

Why did U.S. manufacturing productivity stop growing after 2010? Productivity growth actually disappeared, from an annual rate of +3.3 per cent during 1987-2010 to -0.3 per cent from 2010 to 2023. This article shifts attention from 2010 as the start of the productivity growth slowdown to a decade earlier when output stopped growing. This cessation of output growth in 2000 is attributed to the invasion of imports that closed domestic plants, destroyed jobs, and squeezed profits. After 2000, a chain of causation followed that ultimately undermined productivity growth — from falling capacity utilization, to lower investment in fixed capital and research and development, and an erosion of innovation. Beyond the import invasion, the disappearance of productivity growth is also attributed to a general phenomenon of diminishing returns to innovation, the feeble influence of robots, government regulations that distorted investment, and a shrinking supply of skilled labour in the face of increasing skill demands.

1. Introduction

While the manufacturing sector produces only 10 per cent of U.S. gross domestic product (GDP), it accounts for more than half of U.S. research and development (R&D) and produces most of U.S. exports, fixed investment, and consumer goods. Yet the former dynamism of that sector appears to have vanished. The growth rate of labour productivity in U.S. manufacturing in official data — produced by the Bureau of Labor Statistics (BLS) and Bureau of Economic Analysis (BEA) — was 3.3 per cent per year over the 23 years between 1987 and 2010. But then growth disappeared, registering a negative rate of -0.3 per cent over the following 13 years between 2010 and 2023.1 The vanishing of productivity growth in U.S. manufacturing raises deep questions about the historical core of American prosperity.

How could productivity growth in the entire manufacturing sector completely disappear? Has U.S. manufacturing lost its ability to compete? A substantial literature has emerged that examines numerous possible causes of the productivity slowdown. But those papers contrast productivity growth before and after 2010, with little or no attention to profound changes that occurred before 2010. Yet the deep malaise of U.S. manufacturing began at least a decade earlier. While productivity growth was zero after 2010, manufacturing gross output in the year 2000 began a 23-year interval of zero annual growth.2 That is, the level of manufacturing gross output (which includes the value of intermediate inputs) was the same in 2023 as in 2000, while the level of real GDP (which nets out the value of intermediate inputs) was 57 per cent higher, a stunning contrast.

By what channels does a flood of imported goods undermine the efficiency and viability of domestic manufacturing firms? We find that there is a strong negative correlation across the 19 three-digit manufacturing industries between the post-1987 rise in import penetration and the subsequent post-2000 stagnation of domestic output. Foreign competition not only causes plant closures in the most affected industries like furniture, textiles, and apparel, but squeezes profits throughout other parts of the manufacturing sector, thus cutting funding for fixed investment as well as R&D. There is a striking shift from positive to negative growth of investment after 2000 in many manufacturing industries. Further, when innovation originates from foreign producers of imports, domestic firms lose touch with leading-edge technology, are less able to achieve their own technological advances, and are less able to obtain critical inputs from domestic sources.

There are limits to the import/offshoring explanation of the productivity growth slowdown. By 2018, import penetration (defined as imports divided by imports plus domestic production) had reached 30 per cent or above in half of the manufacturing industries. Averaged across the 19 industries, import penetration increased from 13 per cent in 1988 to 28 per cent in 2018; in the latter year import penetration ranged all the way from 5 per cent in petroleum to 97 per cent in apparel. Yet the productivity growth slowdown was larger for petroleum than for apparel, suggesting that offshoring and imports provide only a partial explanation of productivity growth patterns.

We broaden the investigation by examining symptoms of a deeper malaise that extends beyond manufacturing into the rest of the American economy. A recent New York Times editorial reports decades during which the American shipbuilding industry has delivered ships billions of dollars over budget, years behind schedule, that fail to perform as specified. The U.S. aircraft industry takes 12 years to deliver a new military fighter or bomber. “America’s defense industry, like much of the economy, has lost the ability to build quickly and effectively” (New York Times Editorial Board, 2025).

This article begins with measurement issues. A recent paper by Atalay et al. (2025) convincingly argues that the Producer Price Index (PPI) used by the BEA to deflate output in a given category of goods systematically rises faster than the corresponding Consumer Price Index (CPI), due at least in part to more extensive correction for quality change in the CPI. We incorporate their price adjustments for all of the 19 industries except the computer and electronics industry, where we rely instead on the original research of David Byrne and his coauthors. Because the Atalay-Byrne price adjustments are of roughly the same magnitude before and after 2010, they do not explain any of the productivity growth slowdown, in fact the reverse.

We differ from the previous literature along two other dimensions. Unlike previous papers, including Atalay et al. (2025), that examine the slowdown of total factor productivity (TFP) growth, we focus instead on labour productivity growth, defined as growth in gross output per hour instead of real value-added per hour. Several previous papers have shown that the difference between these two, i.e., intermediate inputs, is subject to “offshoring bias” that can cause the growth of inputs to be understated, and hence the derived growth of value added and TFP to be overstated (Houseman et al. 2011). A second difference with other research is that we choose 2005 rather than 2010 as the break year to define the slowdown for reasons related to the timing effects of the 2008-09 recession.

The article begins with measurement issues and continues with an examination of differences in the magnitude of the slowdown across the 19 manufacturing industries. We then study the channels by which growing import penetration contributed to the cessation of output growth after 2000 and productivity growth after 2010. Next, we examine the sources of declining innovation as a side-effect of shrinking public R&D, changing corporate strategies about private R&D, and the evidence of diminishing returns to R&D in creating innovation. Finally, we examine three additional causes of the slowdown, including the robot puzzle; the role of government regulations in distorting investment and reducing productivity; and the persistent shortage of skilled labour in manufacturing.

2. Measurement: Inflation Bias, Break Date, and Offshoring Bias

2.1 Price Deflator Bias

For many decades economists have demonstrated that price indexes — particularly for durable goods — overstate inflation by failing to take account of quality change and the value of new products. A comprehensive set of new measures of durable goods prices was provided by Gordon (1990). Gradually over the years the BLS has incorporated into its price indexes better measures of quality change, but evidence is not usually available to extend the quality adjustments backwards in time. This leads to a presumption that the extent of upward inflation bias in deflators, and the resulting downward bias in the growth of real output, diminishes over time. Ironically this measurement issue would tend to make pre-2010 productivity growth rates too low, since less accurate price measurement would make pre-2010 output growth rates understated more than their post-2010 counterparts.

A recent attempt partially to address the inflation bias issue has been provided in a much-noticed paper by Atalay et al. (2025). They argue that the BLS devotes more resources to making quality adjustments in the CPI than the PPI and Import Price Index that are currently used to deflate gross output and intermediate inputs. To reduce this quality change bias, the authors carry out the complex task of using input-output tables to match CPI products with specific industries. We accept the Atalay corrections for all of the 19 industries except for the computers and electronic products industry.3 For that we adopt price change corrections suggested by David Byrne based on research by himself and coauthors.4 The Byrne corrections for computers and electronics alter the growth rate of the BEA deflators by -6.9 per cent per year for 1987-2010 and by -5.4 per cent for 2010-23.

For total manufacturing, the CPI substitution raises output growth by 1.6 per cent per year for 1987-2010 and by 1.0 per cent for 2010-23. The adjustments for durable goods are 2.7 and 2.2 per cent respectively, much of which is due to the computer industry. When this industry is excluded the durable goods adjustments drop to 1.8 for both intervals. The nondurable goods adjustments are 1.0 and 0.5 per cent. Except for durables excluding computers, all of these adjustments are smaller for post-2010 than pre-2010, implying that the Atalay revisions do not help explain the productivity growth slowdown at all, but rather make it slightly larger. What they do accomplish is to eliminate, if only slightly, the puzzle of “disappearing” productivity growth in manufacturing, as the 2010-23 productivity growth rate is boosted from -0.3 to +0.7 per cent per year. All productivity growth numbers cited in this article henceforth use only the Atalay-Byrne adjusted data.5

2.2 Implications of Offshoring Bias

As emphasized in the 1996 Boskin Commission report, a source of upward bias in the CPI has long been “outlet substitution bias.” When the price quote for a given product sold at a full-price merchant like Macy’s is replaced by the lower price sold at a rising discount merchant like Walmart, the CPI methodology links out the price decrease and so the benefit to the consumer is not captured in the index. Houseman et al. (2011) identified a parallel price index bias that occurs for the same reason but, rather than involving domestic full-price and discount merchants, instead contrasts intermediate materials previously sold by high-cost domestic producers which are replaced by lower-cost imported materials. The price quotes for the former high-cost domestic producer are not directly linked to the new lower price quote from the foreign supplier. Thus the actual price decline is missed in the deflator for intermediate materials.

This “offshoring bias” leads to an upward bias in the price change of intermediate goods and corresponding downward bias in the growth of real intermediate materials inputs. This matters because real gross output change is based on original data (subject to the price measurement issues discussed above). But everything else in growth accounting is a derived number. If offshoring bias is significant, then the growth of real value added (RVA, that is, gross output growth minus intermediate materials growth) is overstated. Because TFP growth is calculated as RVA growth minus the contributions of capital deepening and labour composition, TFP growth is overstated as well. To the extent that capital input production shifts from domestic to foreign sources, the upward bias in TFP measures is compounded.

Most of the recent literature on the productivity slowdown, including the Atalay paper, focuses on comparisons of TFP growth before and after 2010, and thus is subject to this source of overstatement of TFP growth. Whether this makes the TFP slowdown greater or smaller depends on whether offshoring bias was more or less important after 2010. One approach to assess its impact is to compare the growth of RVA which is altered by offshoring bias and gross output which is not. In our Atalay/Byrne-adjusted data RVA grows faster than gross output by 1.2 per cent per year in 1987-2010 and 0.8 per cent faster during 2010-23, so offshoring bias explains 0.4 annual percentage points of the slowdown in TFP growth leaving aside anything extra from capital deepening. To avoid the inaccuracy introduced by offshoring bias, our article examines only changes in labour productivity defined as gross output per hour and makes no further mention of RVA or TFP growth.

2.3 Break Year

We choose a different break year for defining the slowdown. Most of the recent literature uses 2010 as the break year, comparing 1987-2010 or 1997-2010 with 2010-23. This is understandable, since the puzzle of near-zero productivity growth begins when average growth rates are calculated starting with the 2010-11 annual change. That choice skews the outcome of the slowdown investigation, because the literature generally ignores the fact that the annual rate of change of labour productivity for the single year change of 2009-10 was 8.0 per cent for total manufacturing and 11.6 per cent for durable goods.

Gordon-Sayed (2025) have examined this jump in productivity in quarterly data where the large positive growth occurs in the last three quarters of 2009. Their explanation is that the rapid collapse of output in the fall of 2008, particularly in durable goods manufacturing, led firms to overreact and reduce work hours with a lag by a greater percentage than the decline in output, differing from previous recessions when the percentage change in hours was always less than in output. In their study of the business sector, they show that the “extra layoffs” of 2008-09 and corresponding temporary jump in productivity growth were followed by a rehiring reversal starting in 2010. They conclude that this artifact of the 2008-09 recession leads productivity growth to be overstated in 2008-09 in quarterly data and correspondingly understated in 2010-19 compared to the underlying determinants of trend productivity growth.

To avoid this cyclical distortion, we define the slowdown with 2005 as the break year instead of 2010. Given our desire to avoid any effect of the 2008-09 recession, we could have chosen 2007 instead of 2005. However, 2005 has the appeal that it makes our pre/post slowdown intervals an equal 18 years in duration (1987-2005 compared with 2005-23). The selection of 2005 as the cutoff year is reinforced by the previous research that identifies a structural break in U.S. TFP growth around 2004–2005 (2004Q4), marking the end of the late‑1990s/early‑2000s ICT-driven surge (Fernald, 2015).

The effects of our price adjustment and break year choices are summarized in Table 1. The top frame uses the break year 2010 for the official BEA/BLS growth rates. Two lines are shown for total manufacturing with and without the computer and electronic products industry. All productivity growth rates are defined as the average annual growth rate of gross output for a given interval minus the corresponding growth rate of labour hours.

In the top frame the two growth slowdowns are 3.6 and 2.9 per cent per year, respectively. We will find throughout the article that when the computer industry is excluded the magnitude of the productivity growth slowdown is substantially reduced. The 2010-23 productivity growth rates are negative for both lines in the top frame.

The next frame of Table 1 shows the same growth rates after the Atalay/Byrne price deflator adjustments are applied. The pre/post 2010 growth rates are boosted by about the same amount and so the magnitude of the slowdown is changed only slightly by +0.5 and +0.2 percentage points respectively. That is, the alternative price deflators raise the magnitude of the slowdown for both rows. The post-2010 growth rates of productivity are boosted enough to become positive rates. Thus, the price adjustments “solve” the puzzle of why productivity growth in manufacturing completely disappeared after 2010 but do not shed any light on the magnitude of the slowdown.

The bottom frame of Table 1 calculates the same growth rates when the break year is switched from 2010 to 2005. The growth rates for 1987-2005 are slightly higher than for 1987-2010, simply because the growth rates in the 2005-10 subinterval are lower than the pre-2005 growth rates. But the 2005-10 growth rates are substantially higher than for 2010-23, raising the resulting 2005-23 growth rates by between 0.9 and 0.7 per cent annually compared to 2010-23 for total manufacturing with and without the computer/electronic industry, respectively.

The switch of break dates accomplishes a small part of our goal to explain as much as possible of the productivity growth slowdown. The choice of the 2005 break date reduces the slowdown by 0.6 percentage points for both rows. Overall, the price-adjusted slowdown for total manufacturing of 4.1 percentage points is reduced to 3.5 points by switching the break year, and to 2.5 points by excluding the computer industry. These two changes achieve a 39 per cent reduction in the overall magnitude of the slowdown ((4.1-2.5)/4.1).

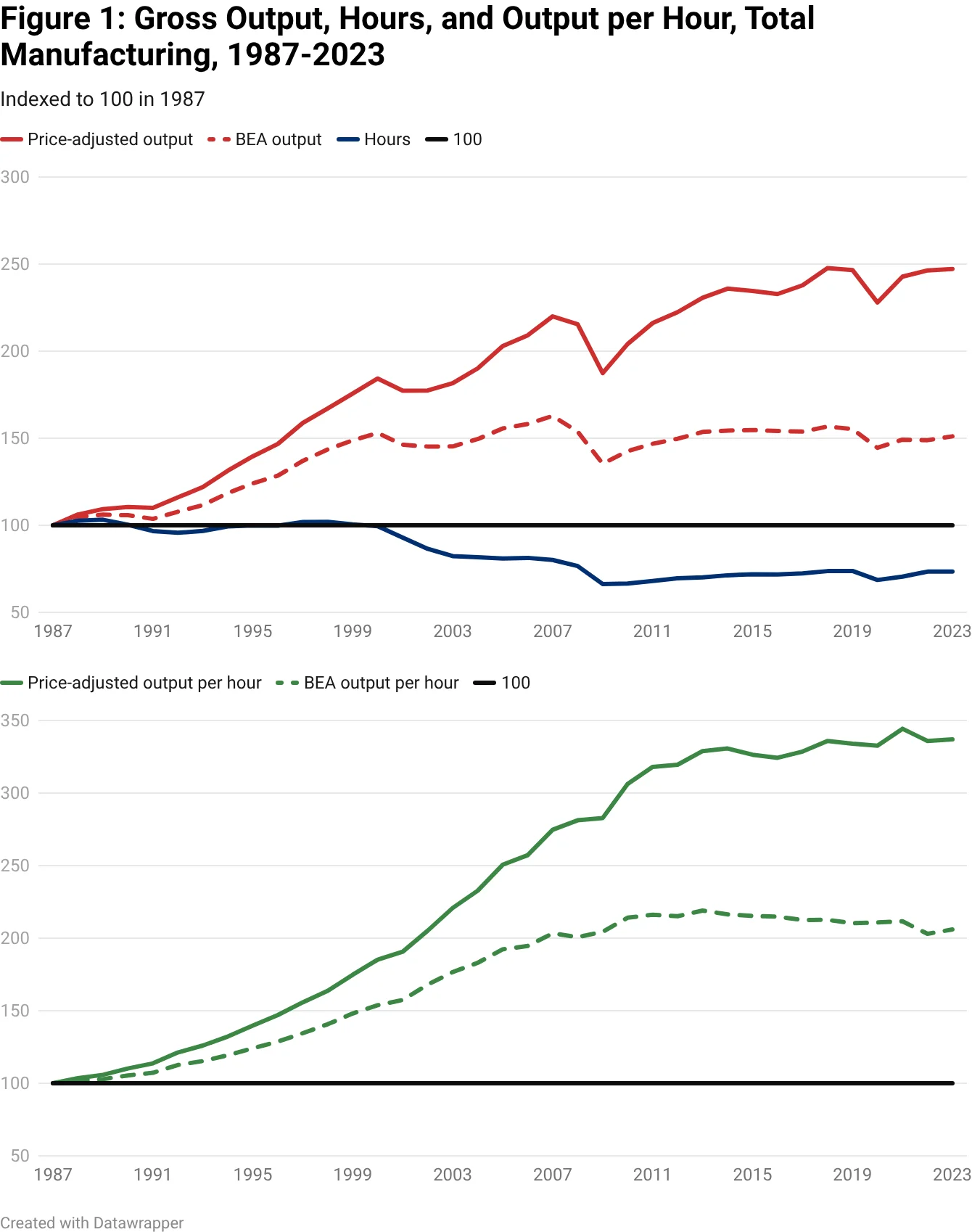

How is the evolution of labour productivity divided between its output numerator and hours denominator? The top frame of Figure 1 displays index numbers (1987=100) for output in red and hours in blue, with the corresponding index number for labour productivity as the green lines in the bottom frame. Dashed lines represent the official BEA/BLS series for output and productivity, while the solid lines plot the series after applying the Atalay/Byrne price adjustments. By depicting the year-by-year evolution of the data, Figure 1 provides additional insight into the timing of the phenomena that we need to explain.

The previous literature has focused on the post-2010 productivity growth slowdown but has generally not noticed another stark slowdown ten years earlier, that of output growth after 2000. The official BEA output series, shown by the dashed red line, stagnates after 2000, with a 2000-23 annual growth rate of -0.1 per cent, sharply down from the 3.3 per cent annual growth rate that occurred during 1987-2000. The price adjustments raise the 2000-23 growth rate of output slightly to a positive 1.3 per cent per year, but the sharp downturn from 1987-2000 to 2000-23 is roughly the same, from 4.7 to 1.3 per cent. We shall return to the theme below that the seeds for the near-disappearance of productivity change after 2010 were planted a decade earlier in 2000 when the import invasion began to swamp domestic industries.

Figure 1 also shows that the 2000-10 decade was different from either pre-2000 or post-2010. The price-adjusted output series shown by the solid red line grew at only 1.0 per cent per year, while employment collapsed, registering an annual growth rate of -4.0 per cent per year. Thus, the apparent similarity of productivity growth in 1987-2000 and 2000-2010, 4.7 and 5.0 per cent respectively, disguises a stark change from healthy output growth and stable employment before 2000 to stagnant output and rapidly collapsing employment during 2000-10. To the extent that the surge of imports caused the post-2000 transition, plant closings of low-productivity plants changed the mix within those industries to higher productivity plants and firms. This is part of the reason that productivity growth remained positive after 2000 through 2010. We return to this theme below.

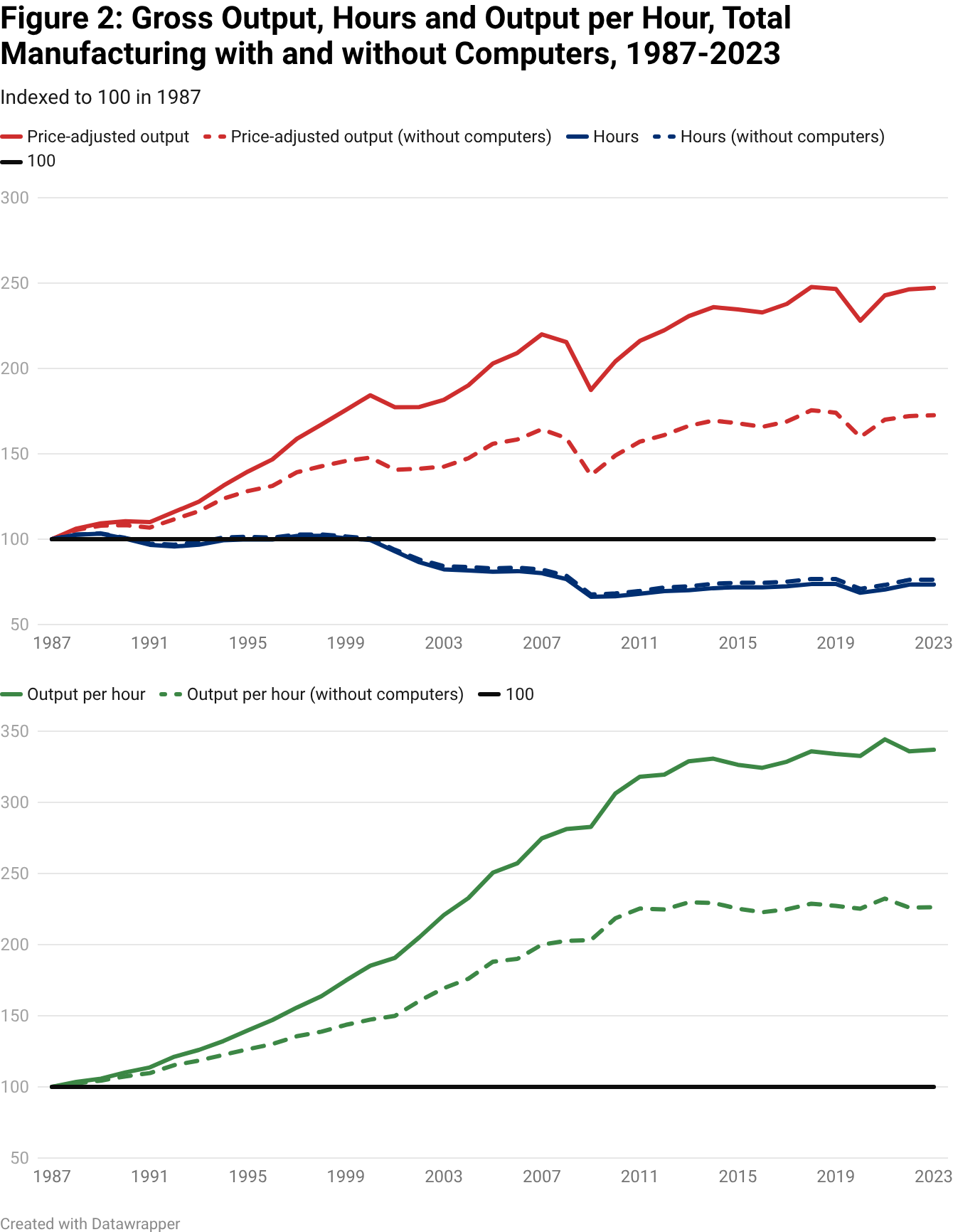

In Figure 2 the solid lines are the same as in Figure 1, while the dashed red and green lines plot the price-adjusted index numbers for output and productivity when the computer industry is excluded. The most important element of Figure 2 is the dashed red line showing that when computers are excluded, output stagnated after 2000, achieving an annual growth rate between 2000 and 2023 of only 0.7 per cent per year after growing at 3.0 per cent per year during the 13 years prior to 2000. For the 2000-10 decade this measure of output growth was 0.1 per cent per year. Thus for 18 of the 19 manufacturing industries the phenomenon of complete stagnation of output growth after 2000 remains valid even with the price adjustments and becomes one of the most interesting facts that needs to be explained. To what extent does the import invasion explain this output stagnation, and does the disappearance of output growth help explain, in turn, why productivity growth transitioned after 2010, when prices are adjusted and computers are excluded?

The lower frame in Figure 2 contrasts the index of manufacturing productivity with and without computers. With the 2010 break date excluding the computer industry explains 24 per cent of the productivity growth slowdown, while using the alternative 2005 break date, the computer contribution is an almost identical 29 per cent.6 Using conventional BEA/BLS data and a 1997-2023 time span with a 2011 break year, a recent report by Chittoor et al. (2025), found a computer industry contribution of 16 per cent.

3. Dimensions of Difference

If the productivity growth slowdown were accounted for by just a few industries and not by the rest of the 19 three-digit industries, then we could focus on a limited set of causes unique to those industries and not to others. But that approach does not work for the U.S. manufacturing productivity growth slowdown, because every one of the 19 industries experienced a post-2005 slowdown in labour productivity growth.

The price-adjusted productivity growth rates for 1987-2005 (dark blue bars) are contrasted with 2005-23 (light blue bars) in the twin charts of Figures 3 and 4. The magnitude of the slowdown is visible as the difference between the length of the dark and light blue bars. Durable goods industries are shown in Figure 3, and the computer industry is excluded to avoid distorting the scale. The ten durable goods industries in Figure 3 are ranked in descending order of the post-2005 slowdown.

An interesting feature of the ranking in Figure 3 is that the industries at the bottom with the smallest slowdowns achieved this standing not just because their productivity growth was higher after 2005 but because it was lower before 2005. On average the bottom four industries slowed from a pre-2005 growth rate of 4.4 per cent to a post-2005 growth rate of 3.2 per cent, or a slowdown of 1.2 per cent. In contrast the four industries at the top of Figure 3 had a higher average pre-2005 growth rate of 4.9 per cent and lower post-2005 growth of 1.5 per cent, resulting in a slowdown of 3.4 per cent per year. A noticeable difference is that most of the industries at the top of Figure 3 with the largest slowdowns produce relatively complex products, including electrical equipment, machinery, and autos, while most of the industries with smaller slowdowns at the bottom of the figure produce relatively simple products, such as primary metals, nonmetallic mineral products, and wood products.

Figure 4 shows the same display for nondurable goods. Here the pattern is different, with all nondurable industries having productivity growth rates close to zero for 2005-23, so that the chart’s ordering by slowdown rank is the same as the rank of 1987-2005 growth rates. The only exception is the food industry, which had very slow pre-2005 productivity growth and negative growth post-2005. For the nondurables in Figure 4 it is hard to discern any relationship between the slowdown by industry and the complexity of that industry’s products. The largest slowdown was in the petroleum and coal products industry, which experienced a remarkable 6.0 per cent slowdown (between 6.0 per cent growth pre-2005 to -0.1 growth post-2005).

While production in petroleum refineries is relatively complex with a large capital investment required, the next two ranked industries – textiles and apparel – are not capital intensive nor complex. These two industries are the poster children of the import invasion, particularly apparel where the import penetration ratio had reached 97 per cent by 2018. Apparel productivity growth during 1987-2005 appears to be at a relatively healthy 5.1 per cent, but that rate was achieved only because hours disappeared at a much faster annual rate (-6.9 per cent) than output (-1.8 per cent). Apparel productivity growth declined to 0.9 per cent after 2005.

The computer and electronic products industry was omitted from Figure 3 due to its extended horizontal scale and is shown separately in Figure 5. The top four bars trace its steady decline in productivity growth from 19.4 per cent during 1987-2000 to 7.2 per cent in 2010-23. Next on the chart are the dark and light blue bars recording the decline in productivity growth from 18.7 during 1987-2005 to 9.4 per cent in 2005-23. The bottom pair of two bars show the difference made when the Byrne price adjustment is excluded and we return to the original BEA/BLS growth rates that are 6.5 and 6.3 per cent slower, respectively.

The stark 9.3 per cent post-2005 decline in productivity growth for the computer industry has rightly attracted more attention than in any other manufacturing industry. We return below to Moore’s Law and its evolution over time along with other factors related to import competition that help as explanations. Here we note that, second only to the 97 per cent of the apparel industry, by 2018 the import penetration ratio for the computer and electronics industry had reached 84 per cent. The decline of this industry is inseparable from its mass offshoring migration to Asia.

4. The Import Invasion and Its Implications

Our primary focus is on the effects of import competition starting in the late 1990s as an important explanation of the productivity growth slowdown that is usually interpreted as starting a decade later. Figure 6 illustrates the expansion of imports from China, Mexico, Canada, and the rest of the world not as a percentage of all imports, but rather as a percentage of domestic U.S. manufacturing output. The import measure encompasses both intermediate goods and final goods that physically arrive in the United States. These ratios are shown for 1991, 2000, 2010, and 2023. Using the abbreviations IM for nominal imports and GO for nominal gross output, the import ratios in Figure 6 are IR = 100*IM/GO.

Figure 6 shows that for all countries the IR increased between 2000 and 2023 from 28 to 45 per cent.7 The decade 2000-2010, when so many domestic manufacturing jobs were destroyed, deserves the term “China Shock,” in the sense that the IR for China more than tripled during that decade, growing by 5.4 per cent of U.S. manufacturing output. China alone accounted for slightly more than half of the 10.1 percentage point increase in the IR for all countries during that decade. By comparison the Mexico IR in the same decade increased by only 1.4 percentage points. By 2023, however, the Mexico IR ratio increased by another 2.4 points from 2010 while the China ratio actually decreased by 1.4 points, and Mexico achieved the distinction of becoming the top importer to the United States.

4.1 Import Invasion and Output Stagnation

We can validate the role of rising imports as a major explanation for the disappearance of output growth after the year 2000. As shown in Figure 2 above, for the 18 industries excluding computers and including the price adjustments, the annual growth rate of output declined from 3.0 per cent per year in 1987-2000 to 0.1 per cent in 2000-10. Was the transition to post-2000 output stagnation related to the import invasion? The 2000-10 growth rates of output in the 18 industries are significantly negatively correlated with the rise of the import penetration ratio in each industry. The correlation coefficient is -0.69 of the individual industry 2000-2010 output growth rates with the 1989-2005 change in the IP ratio, and this is significant at the 1 per cent level.

The import surge not only reduced output growth in the 2000-10 decade and decimated hours and employment, but it had other effects as well on investment, R&D, and the pace of innovation. The displacement of domestic demand was the most obvious of these channels. Standardized goods impacted by low-cost foreign competition were purchased by consumers looking for the lowest prices, and in industries like textiles, apparel, toys, consumer appliances, and furniture, the demand for domestic production melted away. Between 2000 and 2010 output fell by 71 per cent in the domestic apparel industry, by 50 per cent in textiles, 38 per cent in furniture, and 33 per cent in electrical equipment and appliances.8

Not just in these most-exposed industries but in many others, import competition exerted intense pressure on prices and profit markups. Feenstra and Weinstein (2017) document the downward pressure on markups after 2000. Declining markups and profits directly reduce the resources available for capital investment and R&D, thus creating an indirect channel of causation from expanding imports to a decline in capital deepening and innovation.

Many firms responded to this profit pressure by offshoring the supply chain to reduce costs, in addition to their cost-reducing reductions of employment. This in turn resulted in the offshoring bias, as discussed above. As we have seen this leads to the overstatement of growth in RVA and TFP. Since most of the offshoring bias occurred during the 2000-10 decade, it raised the growth rate of TFP during that decade more than after 2010. This implies that studies of the TFP growth slowdown that use a 2010 break date (like Atalay et al., 2025) overstate TFP growth pre-2010 relative to post-2010 and thus exaggerate the magnitude of the TFP slowdown. This occurs in addition to the overstatement of the post-2010 slowdown caused by the 2009-10 cyclical distortion discussed above.

4.2 Reallocation and the 2000-10 Productivity Surge

We previously noted in the context of Figures 1 and 2 above that growth in both output and hours slowed by the same amount between 1987-2000 and 2000-10, implying that productivity growth exhibits no slowdown between those two intervals. But after 2000 the manufacturing economy suddenly shifted gears from healthy output growth with stable hours, to a very different regime of stagnant output with evaporating hours. Autor et al. (2013) explain why the employment decline was so persistent. Many of the plants most affected by the import invasion were located in relatively small cities and towns with few alternative employment opportunities. Displaced workers often could not afford to move, in part because the closing of the local factory decimated the local housing market and evaporated home equity, preventing moves to higher-cost locations.

The post-2000 transition changed the main source of productivity growth from innovation and capital deepening to reallocation when low-productivity plants closed and the mix within firms and industries shifted to higher productivity plants and firms. This mechanism is validated both theoretically and empirically by Bernard et al. (2006). The gain in productivity observed in our industry data does not represent healthy innovation but rather the closing of low productivity plants and the shift in production to higher efficiency plants. These authors document the impact of trade on the closing of inefficient plants. While productivity growth, whether through rising output or falling labour input, is not a concern in and of itself, efficiencies gained from mass closures of domestic plants pose welfare concerns for affected regions. Not only did single plants close but so did entire firms in the textile, apparel, and furniture industries, as well as such iconic firms as RCA and Zenith in consumer electronics. Melitz (2003) provides additional evidence on the intra-industry reallocation effect.

Bloom, Draca, and Van Reenen (2016) found the same effect in Europe, where a similar wave of Chinese imports caused inefficient plants to close and the more efficient plants to restructure, often by shedding labour. Kim (2019) reported a similar finding with the firm-level data in the Canadian manufacturing sector that showed rising import penetration from China shifting economic activities towards high productivity firms which offset the declines of TFP within firms. Thus, both in Europe and North America productivity growth during 2000-10, which appears to provide evidence of continuing healthy innovation as before 2000, actually may have been partly or largely due to plant closings and compositional effects. Since our data are totals for each of the 19 industries without intra-industry firm detail, we cannot measure the within-industry reallocation effects. There is little cross-industry correlation between the post-2000 change in output or productivity growth and the level of 2000 output per hour, indicating that the reallocation effect occurred within industries rather than between industries.

4.3 Investment, R&D, and Innovation

Competition from imports squeezed profits not only in the most exposed industries but throughout manufacturing. The negative impact on domestic investment was augmented by uncertainty and the increasingly attractive option of offshoring production and supply chains. Autor et al. (2020) document that firms most exposed to imports were most likely to reduce capital expenditures. By choosing not to invest in the newest and most efficient automation and manufacturing technologies, these firms lost the chance to implement innovations that were occurring in their particular industries.

As discussed above in our summary of Figure 1, the average annual growth rate of manufacturing output (including computers and price adjustments) slowed from 4.1 per cent in 1987-2005 to 1.3 per cent in 2005-23. Over the same period the average growth rate of real investment declined by about the same amount, from 5.0 to 1.0 per cent per year. Pierce and Schott (2017) highlight the role of the post-2000 Chinese import explosion in reducing investment in the subset of industries most exposed to import competition. Offshoring of the production process also played an important role in declining investment. A large literature on trade (Bernard, Jensen, and Schott, 2006; Acemoglu et al., 2016) documents that increasing imports led to a decrease in capacity utilization and lowered the necessity of additional capital investment within the U.S.

Another cause of lower investment growth in the early 2000s can be traced to the increasing financialization of the U.S. firms. Lazonick (2014) argues that corporations shifted towards a “downsize-and-distribute” regime that redirected earnings to financial interests instead of investment in production capacities, a trend that took off especially after the 2003 Securities and Exchange Commission rule change that made stock repurchases easier. Gutiérrez and Philippon (2017) show that 80 per cent of the decline in investment after 2000 can be accounted for by the amount firms spend on share buybacks.

The process by which low-cost import competition reduced investment had a similar effect on domestic R&D. Industries such as consumer electronics and primary metals shifted R&D activities abroad or concentrated them in large multinational firms that located R&D facilities in foreign countries rather than in the United States. There was also a process by which innovation shifted out of manufacturing to firms in the information technology industry like Apple, which developed software in Silicon Valley and other domestic locations while outsourcing the implementation of manufacturing process innovation to the Asian locations where the hardware device production was concentrated.

Using pre-2007 data from manufacturing patenting, Autor et al. (2020), show a decline in U.S. inventors’ patenting between 2000 and 2007 (which is the end of their sample period) can be linked to import competition. They find that this exposure leads to a decline in private firms’ R&D expenditure and a decline in patent applications. However, it is not clear that offshoring necessarily leads to fewer innovations. The authors also find that the negative impact of imports on innovation performance is larger in less profitable and less capital-intensive firms.

More broadly there are three possible reasons why offshoring may lead to a decline in manufacturing productivity growth. First, offshoring renders researchers and engineers unfamiliar with the manufacturing process, hindering further innovation. As the vice president of General Electric bluntly puts it in an interview with MIT Technology Review (2012), “you can design anything you want but if no one can manufacture it, who cares?” Consequently, offshoring is not simply moving low-skilled jobs abroad, but also makes “businesses dependent on someone else’s innovation for next generation products.” Leveraging an unexpected bilateral trade deal between U.S. and China in 1999, Bena and Simintzi (2025) find that offshoring reduces the willingness of firms to develop labour-saving technology for existing products.

Second, import competition also leads to a reallocation of researchers from manufacturing to service industries. Xu and Gong (2017) identify 47 science and engineering occupations. They find that for research occupations more exposed to import competition, researchers tend to shift from manufacturing to service industries (finance, personal services, business and repair services). For example, one standard deviation increase in occupation-level import competition leads to an 11.5 per cent increase in the share of researchers working in business and repair services.

Third, even if import competition reallocates research effort to firms with more market power, it does not always follow that more dominant firms become more efficient, and smaller, less efficient firms exit the market. There has been a decline in business dynamism in the US, and the dominant firms may have become less efficient over time (Gutierrez and Philippon, 2020; Covarrubias et al., 2019). Decker et al. (2016), show that within the manufacturing sector, the contribution of labour reallocation to TFP growth has declined.

4.4 Outsourcing of the Computer Industry to Asia

As we have seen, the import penetration ratio of the computer industry (NAICS 334) in 2018 had reached 84 per cent, almost as high as low-tech apparel at 97 per cent. The departure of the U.S. industry with the most rapid rate of productivity growth is a central element in the process by which the import tsunami reduced productivity growth in U.S. manufacturing. While the offshoring of apparel, furniture, toys, and other basic consumer products was primarily due to lower labour costs abroad, the surrender of the computer industry is a more complex tale, combining technological shifts, under-investment, U.S. managerial priorities and shortsightedness, and scale effects as ever-increasing Asian production further reduced costs through economies of scale while the reverse process took place in the residual production that remained in the United States.

The primary driver of computer offshoring, unlike the case of apparel and toys, was not low labour costs. Dedrick, Kraemer, and Linden (2010) have shown that labour represents only about five per cent of the cost of manufacturing computer hardware. The offshoring of computer production bears some similarity to the auto industry, where in the 1980s Japanese firms pioneered the “just-in-time” production system that produced automobiles that were not just less expensive but were of higher quality and were more reliable.9 Asian makers of computer components excelled in “process engineering.” Firms in Japan, South Korea, and Taiwan learned to excel at continuous improvement, rapid defect detection, and tight tolerances. Additional sources of electronics offshoring to Asia include government subsidies, the geographical clustering of the supply chain, and greater support for worker training.

5. Innovation and Diminishing Returns

5.1 Declining Innovation

The diminished contribution of innovation to productivity growth can be divided into three separate causes, all involving R&D. The first is the decline of public research, the second the retreat of corporate research from basic science, and the third and perhaps most important, decreasing returns to R&D investment. This set of factors is particularly important for understanding the manufacturing slowdown, since that sector of the economy accounts for two-thirds of R&D expenditure and the related problems are more acute in manufacturing than in the rest of the economy.

Public R&D expenditure declined steadily from its peak of 2.0 per cent of GDP in 1964 to only around 0.7 per cent of GDP in recent years. Gruber and Johnson (2019) argue that revitalizing public research is crucial for future productivity growth, based on the traditional role of positive externalities. In contrast private firms often shun long term projects that are potentially beneficial to society. For instance, Pfizer terminated its R&D efforts on Alzheimer’s and Parkinson’s diseases in early 2018, not because of a lack of funds, but because the patent protection period was too short for the firm to make a profit. In contrast, public research has a long-term horizon. Azoulay et al. (2019) and others point to the army-sponsored Advanced Research Projects Agency (ARPA) which has played a substantial role in the early stages of high-profile inventions, including the internet, personal computers, lasers, and Microsoft Windows.

The decline in public research was aggravated by the retreat of corporate research. Arora et al. (2019), emphasize that U.S. research prior to the 1980s was characterized by giant corporate labs, such as the Bell Lab of AT&T, and research units of DuPont and Xerox, all of which were manufacturing firms. These corporate research clusters focused on general purpose technologies and worked across disciplines on a large scale. However, large companies shifted from general basic science to narrow commercial development starting in the 1980s. As Arora et al. (2015) show, companies became less willing to invest in basic science in part because the results could benefit business rivals.

In recent years attention has shifted to the third factor, diminishing returns to research investment. This in part reflects the influence of a much-cited paper by Bloom et al. (2020), claiming that “new ideas are getting harder to find.” Their two main examples are the development of new drugs by pharmaceutical companies and, for computers, Moore’s Law showing that the number of transistors on a semiconductor chip doubles every two years. The steady exponential growth embodied in Moore’s law has required an increase in the number of research workers by a factor of 18 over the previous four decades.

5.2 Fading Pharmaceuticals

Our 19-industry database covers three-digit industries including chemicals (NAICS 325) but not four-digit industries including pharmaceuticals (industry 3254). BLS (2018) shows that this four-digit industry makes the fourth-largest contribution to the manufacturing TFP slowdown from 1992-2004 to 2004-2016. Growing R&D costs and a higher termination rate of projects are two prominent corollaries of the slowdown. Anticipating in part the Bloom et al. (2020), research, Deloitte (2018) estimates that the average R&D costs of developing a compound from discovery to launch almost doubled from 2010 to 2018.

The slowdown in pharmaceutical innovation may have started much earlier. Gordon (2016) notes that the decades between 1940 and 1970 witnessed the invention or the widespread usage of many important drugs and medical techniques (such as an array of antibiotics, computed tomographic imaging, polio vaccine, and many others), but the rate of innovation slowed down in the decades that followed. Bloom et al. (2020), provide empirical evidence that the research productivity in medical research, defined as the ratio of years of life saved to the number of publications, first increased from 1975 to the mid-1980s and then fell. These authors measure the average annual growth rate of research productivity to be -0.6 per cent for all cancers, -6.8 per cent for breast cancers, and -3.7 per cent for heart disease. The same authors show that lives saved per million in clinical trials per real dollar of research expenditure fell over the same period by a factor of eight for breast cancer research and by a factor of 16 for all cancer research. More recent research has christened “Eroom’s Law” (Eroom = Moore spelled backwards); this shows that drug approvals per billion dollars of real research expenditures declines by half every nine years. Taking the results for computers and pharmaceuticals together, they imply that 60 per cent of total manufacturing R&D expenditure is suffering from diminishing returns.

A straightforward cause of this phenomenon is that it has become increasingly challenging to improve the understanding of basic science. The lab-based process of discovering new drugs and compounds makes it challenging to predict the behavior of materials and requires multiple lab experiments which are costly, time-consuming, and unpredictable. Further, chemical companies face an increasing number of long-term disruptions in the form of more foreign competition, rapid shifts in end-market demand and a growing burden of environmental regulation.

5.3 Automobile Recalls Reduce Productivity

A higher frequency of car recalls since 2012 has reduced industry productivity growth. The cause of increasing recalls may be the increasing complexity of vehicles (Harbour et al., 2015). In addition, researchers at McKinsey conjecture that since many companies now have common product platforms and supply-chain partners, one defect on a single module can negatively affect multiple vehicle models (Aragon et al., 2019).

Auto recall services, if they cannot be carried out by dealer service departments, negatively affect car manufacturers’ productivity, since the factories have to make replacement parts, which raises labour costs and labour input for a given number of vehicles produced. Moreover, car recalls can be costly in themselves. For example, in 2016, GM recalled 23 million vehicles in the U.S. which cost GM $4.1 billion; in 2015, automakers and their suppliers together paid $17.5 billion on claims and warranty accruals (Automotive News, 2018). This issue relates to our previous comments about the persistent low reliability scores of automobiles produced by American-owned firms as tallied by Consumer Reports.

5.4 Productivity Shrinkage in the Food Industry

As shown in Figure 4 above, the food and beverage industry has recorded negative -1.5 per cent annual productivity growth since 2005. Day-Rubenstein and Fuglie (2012) argue that in recent years, new product development has been driven by consumer demand, as opposed to reducing costs or reducing resources needed for production. “An estimated 20,000 new food products are introduced in the U.S. annually. While some of these new products embody technical change, only about 10 per cent are thought to be true innovations. The average lifespan of a new food product is relatively short.”

6. A Catalog of Causes

In addition to resulting from the import invasion and a slowing of innovation, the productivity growth slowdown in U.S. manufacturing has additional causes. Further contributing factors include (1) the failure of robotics to boost productivity growth in the industries where the population of robots has expanded rapidly, (2) environmental and other government regulations, and (3) a persistent shortage of skilled labour. In this section we identify these causes and provide examples for the six industries that make the highest numerical contribution to the post-2005 productivity growth slowdown: computers, petroleum, pharmaceuticals, autos, machinery, and food. Together these six industries explain 71 per cent of the post-2005 slowdown.

6.1 Robotics and Automation

The use of robots expanded rapidly in the past 15 years in some manufacturing industries but did not prevent them from recording zero or minimal productivity growth. Why did the increase in the adoption of robotic technology fail to boost productivity growth? The first answer is the most important. Despite its continued growth, robotics accounted for only 1.1 per cent of total equipment investment expenditure in the manufacturing sector in 2021 (Annual Capital Expenditure Survey). Thus, the gains from robotics automation were swamped by other factors such as lower output demand or falling utilization or required responses to regulations, all of which tended to mask the effect of added robots.

What are the other reasons why robots have had a disappointing effect on manufacturing productivity growth? Based on the task-based model of Acemoglu and Restrepo (2019), numerous articles have shown that increased robot use raises labour productivity. Graetz and Michaels (2018) find that increased adoption of robots from 1993 to 2007 contributed 0.36 percentage points to annual labour productivity growth using panel data of seventeen countries. Acemoglu and Restrepo (2020) use the same data but focus on the U.S. labour market and find that one more robot per thousand workers reduces the employment-to-population ratio by 0.2 percentage points, which seems to match the narrative of the task-based model where automation displaces low- to middle-skill labour.

On the other hand, Benmelech and Zator (2025) find using cross-country and German administrative data that firms invest in robots when they face difficulties in finding workers and subsequently increase employment after the investment. This limits the economic impact of robots. Moreover, a significant portion of the increased robotics use is concentrated in the auto industry, which has mainly invested in robotics to drive its electric vehicle transition and respond to labour shortages (IFR, 2024). Given that the auto industry was responsible for one-third of the annual installations of industrial robots in 2024, it may be that other issues that reduce auto-industry productivity growth have offset the benefits that robots would be expected to provide.

A key challenge in automation is to ensure a smooth integration of new technologies to existing production facilities. Knoess et al. (2017), highlight that automation and robotization do not necessarily lead to productivity gains for all firms. Over the past two decades, the leading auto factories only automate “the simplest, most repetitive processes” such as the paint and body shops where they see the greatest gains from automation.

Skill shortages, which we discuss below, could partly be responsible for the unimpressive productivity impact of industrial robots in recent years. Between 2015 and 2024, the robot density defined as the number of industrial robots per 10,000 workers in the manufacturing sector almost doubled in the United States from 176 to 307, whereas China with its excess supply of STEM graduates saw a ten-fold increase from 51 to 567 within the same period (Müller, 2025). The lack of skilled workers who can manage these robots could be exerting downward pressure on the U.S. robot adoption rate.

6.2 Regulatory Burdens

Regulation changes that may impact productivity growth include tighter environmental laws, stricter pollution controls, and added safety standards. Heavy manufacturing industries such as petroleum, chemicals, and motor vehicles were most exposed to regulations that redirected capital investment or increased compliance costs. The food and beverage industry also faced tighter controls because of increased concern for public health and food safety in recent decades. In contrast the machinery and computer industries were largely unaffected by changes in regulations.

The Clean Air Act Amendment of 1990 called for the reformulation of motor fuels to reduce emissions from motor vehicles, which required firms to process gasoline with a higher percentage of oxygen. Between the late 1990s and early 2000s, EPA significantly expanded enforcement of regulations that discouraged firms from investing in new refineries or modifications to existing refineries as needed for capacity growth. The New Source Review (NSR) program, for example, required permitting before construction or modification of major stationary sources, including oil refineries, to ensure installation of pollution control equipment. NSR enforcement and interpretive uncertainty imposed both delays and cost increases on refinery projects, discouraging capacity expansion and adding permitting burden (Senate Hearing 107-868).

The Food Safety Modernization Act in 2011 was a significant shock to the regulatory framework for the food and beverage industry that changed the regime from responding to food contamination to requiring preventive measures by manufacturers. These included Hazard Analysis and Risk-Based Preventive Controls (HARPC) plans and increased inspection frequency and extra regulatory authority by the FDA. Firms responded to this change by increasing non-production labour for quality control, documentation of plans, and compliance, which would have minimal impact on output expansion. Our price-adjusted data record an output growth rate for the food industry of just 0.2 per cent per year between 2010 and 2023 while capital input increased by 2.1 per cent per year and investment grew by 3.2 per cent. This is consistent with a redirection of investment from the achievement of output and productivity growth to the compliance with regulatory requirements.

The main channel of regulatory consequences on labour productivity of the motor vehicle industry has occurred through changes in the fuel economy and emission standards. The change in the fuel economy standards imposed a binding constraint on auto manufacturers and forced them to enact engineering changes rather than complying through controlling the product mix of passenger cars and trucks. Moreover, added pollution controls required advanced catalytic converters and engine controls which increased vehicle cost and complexity and capital investment without much output effect (Wang and Miao, 2021).

The chemical industry was significantly impacted by the set of regulatory changes after 2000. Firms were required to invest heavily in end-of-pipe abatement, scrubbers, and monitoring systems. A series of papers already studied the effect of environmental regulation on manufacturing productivity. Greenstone, List, and Syverson (2012) use the 1972-1993 plant-level Census of Manufactures data to show that plants located in the non-attainment areas that faced much stricter regulation exhibited lower total factor productivity growth rates than the plants in the attainment areas. They estimate that the organic chemicals industry experienced a TFP decline of roughly 17 per cent. Shapiro and Walker (2018) show that increased regulatory burden on the manufacturing sector through pollution taxes led to abatement investment rather than productivity-enhancing technology development.

6.3 Skill Shortages

The BLS reported for 2025Q3 that more than 400,000 positions in the manufacturing sector remained open and were not filled. A survey by the National Association of Manufacturers (NAM) shows that attracting and retaining talent has been ranked as the primary business challenge consistently since 2017 (Deloitte, 2024). This shortage of skilled workers in manufacturing is not a new phenomenon. Instead, it has developed over the past two decades through the interplay of structural changes in the labour force, educational preferences biased against manufacturing jobs, and the evolving economic environment and advances in technologies.

The skill gap can be dated back to 2001, when 80 per cent of manufacturers reported a moderate to serious shortage of qualified job applicants in a survey by the NAM. This was followed by the earliest wave of retirement of skilled workers in the 2000s who entered the workforce in the hiring boom of the 1970s and 1980s (National Academies of Sciences, 2017). Their exit meant losses in tacit knowledge and skills accumulated over decades, but U.S. firms increasingly stopped training workers internally and shifted the burden of preparing occupational skill and knowledge to schools and students, which widened the skill gap even more (Cappelli, 2015). The Great Recession of 2008-09 also contributed to this trend by permanently altering the skill pipeline, as the entry-level positions disappeared and did not fully recover (Mullins and Forbes, 2015).

In part because of the aging and retirement of the skilled workforce, the supply of qualified workers stagnated. From 2011 to 2022, there was no growth in the number of associate degrees, which prepare graduates for high-skilled trades. More high school students chose to go to college instead of trade schools, as the educational system placed more weight on college attendance. The impression of manufacturing jobs as dangerous or dirty further discouraged students, though these perceptions were often misconceived or outdated (Stockman, 2025). While the supply of skilled workers has stagnated, the demand has continued to expand in response to recent advances in technology and the complexity of machinery. Overall, the difficulty of finding high-skilled workers in recent decades suggests bottlenecks and complications in production processes which contributed to the productivity growth slowdown across so many of the component industries within manufacturing.

The auto industry has been hit hardest in terms of the shortages of skilled labour, especially positions such as industrial maintenance technicians, automation and controls machinists, and tool and die makers. These occupations are difficult to fill as they require a long period of training and combine knowledge from multiple disciplines in mechanical, electrical, and software engineering. With the skill pipeline broken after the Great Recession, manufacturers in the auto industry have consistently reported difficulty in obtaining high-skilled workers for their factories. More recently, another source of skill shortage emerged from a geographic mismatch between areas where internal combustion engine vehicles manufacturing jobs are being lost and where new battery electrical vehicles manufacturing jobs are emerging, which highlights multi-faceted struggles in the search of skilled labour (Saha et al., 2025). Both petroleum and chemicals sectors rely on high-skilled plant operators who facilitate continuous-flow production, which exposes them to the skill shortage problem due to decreases in apprenticeship programs and the retirement of experienced workers. Moreover, the two industries are heavily capital-intensive and safety-constrained, hence the loss of skills in these industries often shows up as lower utilization, not lower employment. The tightened regulations and safety standards in recent years also contributed to the high demand for instrumentation and control technicians who are essential to ensure safe operation under the constraints imposed by environmental rules.

7. Conclusion

Official BEA/BLS measures show that U.S. manufacturing labour productivity growth disappeared after 2010, collapsing from +3.3 per cent per year during 1987-2010 to -0.3 per cent per year between 2010 and 2023, representing a slowdown of 3.6 per cent per year. How could a sector that had propelled American growth since the founding of the Republic stumble so badly into apparent stasis? An emerging literature has attempted to explain this slowdown by changes that occurred after 2010.

This article starts the story ten years earlier. Over the decade 2000-2010 manufacturing employment fell by 44 per cent from 17.3 to 11.5 million. The wave of imports that caused this employment evaporation was christened by David Autor and his co-authors as the “China shock”, but we refrain from using this term because over the longer period 1991 to 2023 China accounted for only 22 per cent of the increase in the ratio of imports to domestic manufacturing output. Reflecting the fact that nations worldwide have increased the penetration of imports into the U.S., we prefer the term “import invasion.”

Just as stark as the disappearance of productivity growth after 2010 was the disappearance of output growth ten years earlier. As one U.S. industry after another witnessed its sales melt in the face of import competition, the response was not just to cut employment and close plants but also to experience a squeeze on profits, a decline in capacity utilization, a decline in investment both in fixed capital and R&D, and indirectly a decline in the pace of innovation. In many cases suppliers of components moved offshore before producers of final goods, leading to emerging gaps in the domestic supply chain. While measured productivity growth during the 2000-2010 decade was the same as during 1987-2000, it occurred in a completely different industry environment. The same productivity growth that in 1987-2000 was the difference between healthy growth in output and zero growth in hours of work, instead in the 2000-10 decade was the same arithmetic difference between stagnant output and evaporating hours.

Our measure of the productivity growth slowdown makes three changes from most of the literature that uses BEA/BLS data to assess the slowdown that begins in 2010. We adjust the deflators of the BEA gross output data by incorporating into our output measures the deflator adjustments proposed by Atalay et al. (2025), to improve the treatment of quality change in existing deflators. These boost the growth rate of output and productivity in total manufacturing and a few durable goods industries, with little effect for other durables and most nondurable goods industries. The switch to these deflators does not help explain the slowdown but rather increases the puzzle, as the price adjustments boost the post-2010 manufacturing productivity slowdown from -3.6 per cent to -4.1 per cent per year.

Our second change is to switch the break date for the slowdown from 2010 to 2005, due to the unusual positive bubble of productivity growth in 2009-10 resulting from recession-caused shedding of labour. This switch in the break year reduces the magnitude of the slowdown from -4.1 per cent when dated as starting in 2010 to -3.5 per cent when the break date is 2005. We join other authors in pointing to the computer and electronic products industry as responsible for a disproportionate share of the slowdown. When measured for 18 of the 19 manufacturing industries, excluding computers, the slowdown declines from -3.5 to -2.5 per cent per year. Thus, we eliminate 39 per cent of the slowdown ((4.1-2.5)/4.1) prior to the start of our substantive analysis. While this might seem to be defining away the problem, the sources of the computer industry slowdown are better understood than for most of the remaining 18 manufacturing industries.

Another difference with some past research is that we focus on labour productivity rather than TFP. A measurement issue called “offshoring bias” leads to an understatement of growth in intermediate inputs. Since value added growth is obtained by subtracting from gross output growth the understated growth in these inputs, growth in both value added and TFP is overstated. Since the offshoring bias was most significant when imports were expanding most rapidly, this implies that the growth in TFP is overstated more before 2010 than afterwards, leading to an exaggeration of the TFP slowdown when 2010 is the break year for defining the slowdown. This source of overstatement of the slowdown is avoided in this article by limiting our attention to labour productivity growth, defined as the growth in gross output per hour.

We examine differences in the post-2005 slowdown across the 19 three-digit manufacturing industries, ranging from -12 per cent per year for computers to -0.2 per cent for wood products. For durable goods the extent of the slowdown is greatest for complex products like computers, autos, electrical equipment, and machinery, and smaller for less complex products like furniture, wood, and nonmetallic minerals. No such pattern emerges for nondurable goods, where the largest slowdowns are for the most capital-intensive industry – petroleum – and the two least capital intensive – textiles and apparel. The fact that 14 of the 19 industries experienced a post-2005 slowdown of more than -2 per cent suggests that the underlying causes of the slowdown are largely common to many industries rather than specific to each industry.

Our discussion of the import invasion establishes a causal chain between the import invasion and the post-2000 disappearance of output growth. Across the 18 industries excluding computers there is a highly significant negative correlation between the post-2000 growth of industry output and the 1987-2005 growth of that industry’s import penetration ratio. We trace a channel of causation from the arrival of imports to declining domestic sales and employment, lower profits and capacity utilization, and less investment in fixed capital and R&D.

The effect of imports on domestic innovation is more complex. Some authors point to a shift of innovation activity toward larger leading firms both inside and outside of manufacturing, in which case innovation shifts its location rather than experiencing a decline. Others argue that domestic manufacturing and innovation are complements; when production of components is offshored the growing distance from the production process inhibits further improvements that combine design and process innovation.

The computer and electronic products industry, which contributed most to manufacturing productivity growth slowdown, largely offshored production to Asia after 2005. By 2018 its import penetration ratio had reached 84 per cent. This did not occur primarily because of lower labour costs, as labour makes up only five per cent or less of manufacturing cost for most electronic products. Instead, the attraction of Asia was its emphasis on process innovation. “Manufacturing optimization” leads to the ability to ramp up production quickly at massive scale. Further explanations include government subsidies, geographically concentrated supplier clusters, and support for worker training.

The article then turns to factors that help to account for the declining contribution of innovation to productivity growth. These include a reduction in public support for R&D, and a shift in emphasis of private R&D from basic science and process improvement to brand extensions and product copying. A third factor is diminishing returns to research effort as demonstrated in recent research that “new ideas are getting harder to find.” Even though Moore’s Law in the computer industry may continue its pace to some degree, the number of research workers needed to maintain that pace has increased multifold in the last four decades. Similarly, a given number of research workers in the pharmaceutical industry produces ever fewer patents, drug approvals, and lives saved.

We emphasize the interplay between investment and regulation. Import competition reduced profits and investment directly. Beyond that regulations and other structural changes diverted investment from improving productivity to adhering to regulatory demands. Auto makers had to divert resources to raising fuel economy and convert to electric vehicles, drug makers had to wait longer for FDA approvals, the chemicals industry faced safety and anti-pollution regulations, the food industry grappled with new safety regulations, and petroleum refineries had to retool to process newly developed fracking supplies and ethanol requirements.

A separate issue involving investment was the apparent failure of the rapidly expanding robot population to boost productivity growth in the auto industry, where robots are most heavily used. One explanation is straightforward – robot investment constitutes only one to two per cent of total manufacturing equipment investment. Another involves diminishing returns – robots are already widely used in auto body and paint shops but cannot yet do sensitive assembly work requiring human hands and dexterity, particularly as electronic controls and devices make autos ever more complex.

Our introduction to this article cited increasing concern at delays and defaults in American industry more generally, from military hardware to infrastructure projects like high-speed rail. Our analysis identifies a combination of failings of government and private industry. The government has retreated from basic research and until recently has abandoned industrial policy that might have created a coordinated effort to match Asian excellence in process innovation. Private corporate research has switched from basic science to duplicative product extensions. Investment in automation and productivity-enhancing capital has been partly set aside by share buybacks and short-term profit maximization. Government and private firms have jointly failed to anticipate a growing shortage of skilled labour and have set up a comprehensive set of training and apprenticeship programs.

Finally, we return to the import invasion. To date, the literature has focused on the post-2010 decline in TFP growth. Equally important was the post-2000 disappearance of output growth. Further study is warranted about intra-industry reallocation from closed plants to more productive plants and firms to explain at least in part why productivity growth continued during the 2000-10 decade, despite the import invasion that eroded the competitiveness of American manufacturing during the same decade. The many issues addressed here support skeptics who doubt that a broad-based regime of tariffs can revive American manufacturing output, employment, and productivity growth. It may already be too late.

References

- Acemoglu D., D. Autor, D. Dorn, G. H. Hanson, and B. Price (2016) “Import Competition and the Great US Employment Sag of the 2000s,” Journal of Labor Economics, Vol. 34, No. S1, pp. S141–S198.

- Acemoglu D. and P. Restrepo (2019) “Automation and New Tasks: How Technology Displaces and Reinstates Labor,” Journal of Economic Perspectives, Vol. 33, No. 2, pp. 3–30.

- Acemoglu D. and P. Restrepo (2020) “Robots and Jobs: Evidence from US Labor Markets,” Journal of Political Economy, Vol. 128, No. 6, pp. 2188–2244.

- Aragon A., U. Huber, T. Möller, and N. Heiko (2019) “Preventing Car Recalls with a Quality Focus,” McKinsey.

- Arora A., S. Belenzon, and A. Patacconi (2017) “The Decline of Science in Corporate R&D,” Strategic Management Journal, Vol. 39, No. 1, pp. 3–32.

- Arora A., S. Belenzon, A. Patacconi, and J. Suh (2019) “The Changing Structure of American Innovation: Some Cautionary Remarks for Economic Growth,” in Innovation Policy and the Economy, Vol. 20.

- Atalay E., A. Hortaçsu, N. Kimmel, and C. Syverson (2025) “Why Is Manufacturing Productivity Growth So Low?” NBER Working Paper No. 34264.

- Automotive News (2018) “Auto Recall Bill Grew 26% to $22 Billion in 2016, Study Says.”

- Autor D. H., D. Dorn, and G. H. Hanson (2013) “The China Syndrome: Local Labor Market Effects of Import Competition in the United States,” American Economic Review, Vol. 103, No. 6, pp. 2121–2168.

- Autor D., D. Dorn, G. H. Hanson, G. Pisano, and P. Shu (2020) “Foreign Competition and Domestic Innovation: Evidence from US Patents,” American Economic Review: Insights, Vol. 2, No. 3, pp. 357–374.

- Azoulay P., E. Fuchs, A. P. Goldstein, and M. Kearney (2019) “Funding Breakthrough Research: Promises and Challenges of the ARPA Model,” Innovation Policy and the Economy, Vol. 19, pp. 69–96.

- Bena J. and E. Simintzi (2025) “Machines Could Not Compete with Chinese Labor,” Review of Finance, Vol. 29, No. 6, pp. 1619–1661.

- Benmelech E. and M. Zator (2025) “Robots and Firm Investment,” Journal of Financial Economics, Vol. 174, Article 104183.

- Bernard A. B., J. B. Jensen, and P. K. Schott (2006) “Survival of the Best Fit,” Journal of International Economics, Vol. 68, No. 1, pp. 219–237.

- Bloom N., C. I. Jones, J. Van Reenen, and M. Webb (2020) “Are Ideas Getting Harder to Find?” American Economic Review, Vol. 110, No. 4, pp. 1104–1144.

- Bloom N., M. Draca, and J. Van Reenen (2016) “Trade Induced Technical Change?” Review of Economic Studies, Vol. 83, No. 1, pp. 87–117.

- Byrne D. M., J. G. Fernald, and M. B. Reinsdorf (2016) “Does the United States Have a Productivity Slowdown or a Measurement Problem?” Brookings Papers on Economic Activity, Vol. 1, pp. 109–182.

- Byrne D. M., A. Hamins-Puertolas, and M. M. Harnish (2023) “Transistors All the Way Down: Viability of Direct Volume Measurement (and Price Indexes) for Semiconductors,” Working Paper.

- Cappelli P. H. (2015) “Skill Gaps, Skill Shortages, and Skill Mismatches,” ILR Review, Vol. 68, No. 2, pp. 251–290.

- Chittoor R., P. Pietraru, and A. Sharpe (2025) “The Stylized Facts of the United States Manufacturing Productivity Slowdown,” CSLS Research Report.

- Covarrubias M., G. Gutiérrez, and T. Philippon (2019) “From Good to Bad Concentration?” in NBER Macroeconomics Annual, Vol. 34.

- Day-Rubenstein K. and K. Fuglie (2012) “R&D and Productivity Lag in Food Manufacturing,” USDA Economic Research Service.

- Decker R. A., J. Haltiwanger, R. S. Jarmin, and J. Miranda (2016) “Declining Business Dynamism,” Hutchins Center Working Paper No. 23.

- Dedrick J., K. L. Kraemer, and G. Linden (2010) “Who Profits from Innovation in Global Value Chains?” Industrial and Corporate Change, Vol. 19, No. 1, pp. 81–116.

- Deloitte and The Manufacturing Institute (2024) Talent Study.

- Feenstra R. C. and D. E. Weinstein (2017) “Globalization, Markups, and US Welfare,” Journal of Political Economy, Vol. 125, No. 4, pp. 1040–1074.

- Fernald J. G. (2015) “Productivity and Potential Output Before, During, and After the Great Recession,” in NBER Macroeconomics Annual, Vol. 29, No. 1, pp. 1–51.

- Food and Drug Administration (2015) “FSMA Final Rulemaking for Current Good Manufacturing Practice.”

- Gordon R. J. (1990) The Measurement of Durable Goods Prices. Chicago: University of Chicago Press.

- Gordon R. J. (2016) The Rise and Fall of American Growth. Princeton: Princeton University Press.

- Gordon R. J. and Sayed (2024) “New Perspectives on Productivity Dynamics in the U.S. Private Economy, 1950–2023,” CEPR Discussion Paper No. 19569.

- Graetz G. and G. Michaels (2018) “Robots at Work,” Review of Economics and Statistics, Vol. 100, No. 5, pp. 753–768.

- Greenstone M., J. A. List, and C. Syverson (2012) “The Effects of Environmental Regulation on Manufacturing Productivity,” MIT Working Paper.

- Gruber J. and S. Johnson (2019) Jump-Starting America.

- Gutiérrez G. and T. Philippon (2017) “Investment-less Growth,” Brookings Papers on Economic Activity, Vol. 48, No. 2, pp. 89–190.

- Gutiérrez G. and T. Philippon (2020) “Some Facts about Dominant Firms,” NBER Working Paper No. 27985.

- Harbour R., M. Hill, and J. Schmidt (2015) “The Harbour Report,” Oliver Wyman.

- Houseman S., C. Kurz, P. Lengermann, and B. Mandel (2011) “Offshoring Bias in US Manufacturing,” Journal of Economic Perspectives, Vol. 25, No. 2, pp. 111–132.

- International Federation of Robotics (2024) “U.S. Companies Invest Heavily in Robots.”

- Ji K., L. Nauta, and J. Powell (2023) “Mapping Global Supply Chains: The Case of Semiconductors,” RaboResearch.

- Jibrell A. (2018) “Auto Recall Bill Grew 26% to $22 Billion in 2016,” Automotive News.

- Kim M. (2019) “Does Import Competition Reduce Domestic Innovation?” International Productivity Monitor, No. 37, pp. 72–95.

- Knoess C., R. Harbour, and S. Scemama (2017) “Prepare Your Workforce for the Automation Age,” Harvard Business Review.

- Lazonick W. (2014) “Profits without Prosperity,” Harvard Business Review, Vol. 92, No. 9, pp. 46–55.

- Melitz M. J. (2003) “The Impact of Trade on Intra-Industry Reallocations,” Econometrica, Vol. 71, No. 6, pp. 1695–1725.

- Mullins J. and B. E. Forbes (2015) “CES Employment Recovers in 2014,” Monthly Labor Review.

- National Academies of Sciences (2017) Building America’s Skilled Technical Workforce.

- New York Times Editorial Board (2025) “America Can’t Make What It Needs for Its Defense,” New York Times, December 14.

- Pierce J. R. and P. K. Schott (2017) “Investment Responses to Trade Liberalization,” NBER Working Paper No. 24071.

- Saha D., R. Shrestha, N. Hunt, and E. Kim (2025) “How US Auto Workers Can Thrive in the Transition to Battery Electric Vehicles,” World Resources Institute.

- Shapiro J. S. and R. Walker (2018) “Why Is Pollution from US Manufacturing Declining?” American Economic Review, Vol. 108, No. 12, pp. 3814–3854.

- Schott P. K. (2008) “The Relative Sophistication of Chinese Exports,” Economic Policy, Vol. 23, No. 53, pp. 6–49.

- Stockman F. (2025) “Why Factories Are Having Trouble Filling Jobs,” New York Times.

- Terry C. and N. Lesser (2018) “Unlocking R&D Productivity,” Deloitte Centre for Health Solutions.

- U.S. Census Bureau (2021) “Annual Capital Expenditures for Robotic Equipment.”

- U.S. Congress (2002) Senate Hearings on New Source Review Policy.

- Xu R. and K. Gong (2017) “Does Import Competition Induce R&D Reallocation?” IMF Working Paper.

- Wang Y. and Q. Miao (2021) “The Impact of Corporate Average Fuel Economy Standards,” Resource and Energy Economics, Vol. 63, Article 101211.

Footnotes

- Labour productivity is gross output from the BEA National Income and Product Accounts “GDP by Industry” tables and hours are from the BLS productivity table “Total Factor Productivity by Major Industries.” The output data are subsequently adjusted below for alternative price deflators.

- The 2000-23 annual growth rate of manufacturing output in the BEA data is -0.05 per cent.

- Chad Syverson kindly provided detailed annual price change adjustments by industry for 1998-2023. We extended these by applying the average adjustment from 1998-2005 uniformly to each year between 1988 and 1997.

- Byrne’s papers provide suggested corrections to BEA deflators for industry 334 for three time intervals: 1978-95, 1995-2004, and 2004-14. We have extended his suggested bias corrections to 2023; details of this translation are provided in the Data Appendix.

- Table 1 that follows compares the two alternative series.